What is LVR and can it affect how much I can borrow?

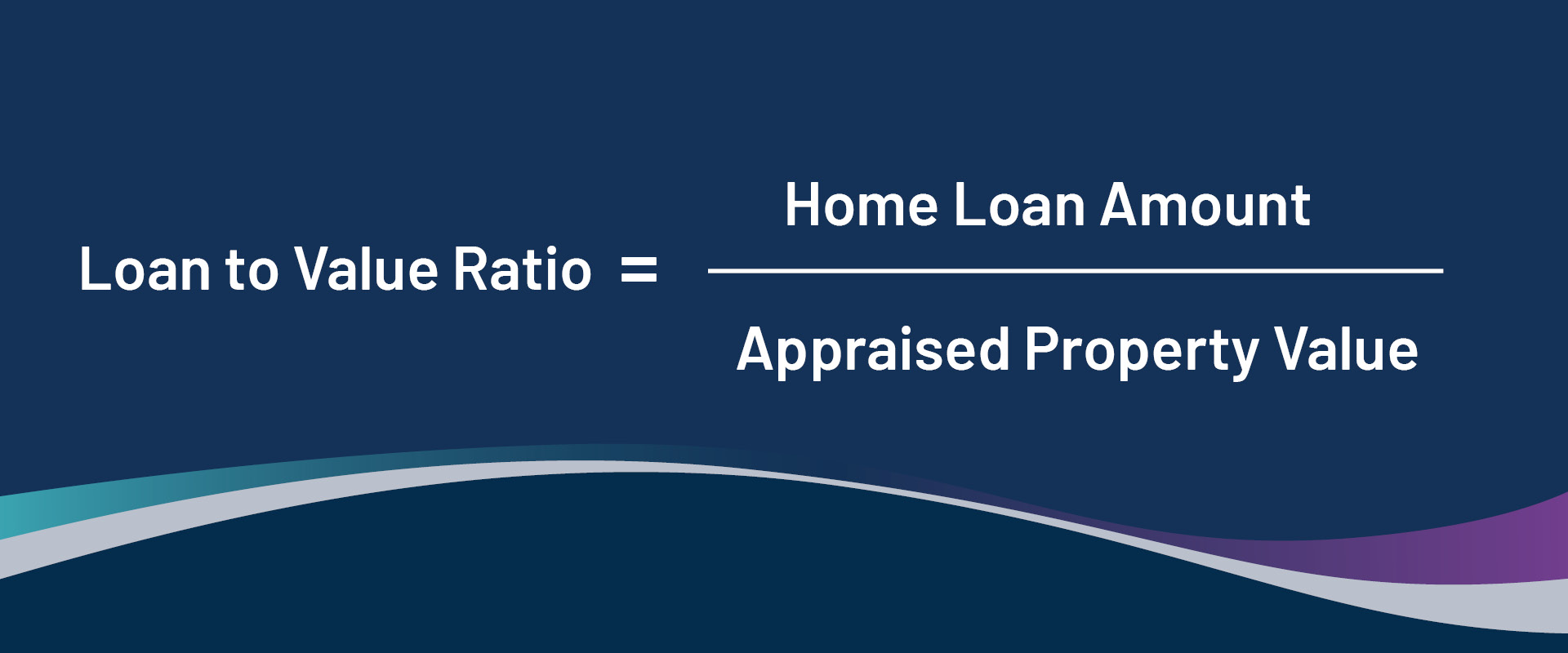

How do I work out my LVR?

To illustrate, let’s say you purchase a property for $500,000 (and the formal valuation figure is the same) and you apply for a $400,000 home loan, the LVR on your loan is calculated as follows:

($400,000 ÷ $500,000) x 100 = 80% LVR

When working out how much you need to borrow, remember to factor in additional fees and costs associated with purchasing a property. You will need enough money to cover stamp duty, inspections and conveyancing fees among others on top of the deposit for your property.

What is maximum LVR?

LVR is one of the factors lenders use to determine the risk associated with a mortgage application. A ratio above 80% may be considered higher risk. In order to reduce some of this risk, most lenders require borrowers with an LVR above 80% to take out lenders mortgage insurance (LMI). LMI protects the lender against default on the loan. This insurance does not protect the borrower, however. If you default on your loan repayments, your lender may foreclose on your property even though you have paid LMI.

Provided you meet certain criteria, you may still be eligible for a loan with an LVR up to 95%. The lender generally looks for things like long term employment, clean credit history and genuine savings. LVR may also be used to determine the interest rate that will be applied to your home loan.

What are LVR restrictions?

In certain situations, a lender may impose restrictions on the maximum LVR. These are typically related to:

- Credit history

If you have defaults on your credit file, your lender may view you as a higher credit risk and cap your maximum LVR accordingly - Type of property

Heritage listed buildings and other unique properties have a limited market appeal and as such, can be difficult for lenders to resell in the event of default - The location of the property

Properties in rural and remote areas and inner-city apartments may incur an LVR restriction due to the lack of demand (or oversupply) which can affect the resale value

What to do if you have a high LVR

It’s fairly common for borrowers to have an LVR of more than 80%. Having a smaller deposit does not put your dream of homeownership out of reach, especially if other factors, like your employment status, credit history, and property type and location are acceptable to your lender.

Contact emoney if you would like more information on LVR or LMI, or you would like to speak to a lending specialist to see how we can help you get a home loan.

First Home Buyer's Guide

Enter your email address for instant access to our handy First Home Buyer's ebook.

Construction Loan Guide

Building a new home. Find out about the construction loan process.